Main Takeaways from the Chapter “Automotive”

In September 2024, the European Commission published a paper titled The future of European competitiveness authored by former ECB president Mario Draghi. The in-depth analysis and recommendations section of the so-called "Draghi Report" devotes an entire chapter to the European automotive industry, examining its transformation and challenges in the context of global shifts toward green mobility, Software-Defined Vehicles (SDVs), and evolving market dynamics. How can SDVs help narrow the growing competitive gap between Europe and emerging markets like China? While the report primarily focuses on the transition to low- and zero-carbon mobility, it also provides valuable insights on SDVs and, implicitly, open source*, which we summarised in this post.

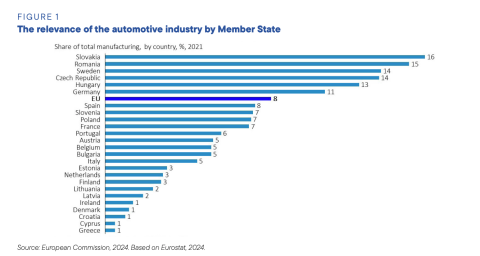

"The automotive sector is undergoing the biggest structural transformation in over a century." This statement on page 141 of the Draghi report encapsulates the core findings of the entire chapter. The report shows that automotive is vital to the EU economy, providing 6.1% of employment and 8% of manufacturing value, with strong export performance. Four out of ten of the world’s biggest automotive companies have their headquarters in the EU.

Competitive Challenges and SDVs

However, competitiveness faces challenges from cost pressures, regulatory demands, and the transition to electric and autonomous vehicles, with SDVs being a key success factor for competitors:

- Production costs in the EU are 30% higher than in China, partly due to energy and labour costs. Apart from automation and robotics, the transition to battery electric vehicles (BEVs) is identified as an essential factor since BEVs are easier to manufacture than traditional ICE (internal combustion engine) vehicles.

- China has surpassed the EU in SDV and electric vehicle (EV) technology and market share, exporting affordable EVs to Europe and dominating battery production. Leveraging substantial subsidies, the Chinese government aims to dominate the global automotive industry, as outlined in various strategic documents (i.e. “Made in China 2025” and its 14th Five-Year Plan). Side note: It’s somewhat ironic that the EU's own ambitious climate policy, designed to incentivise low-carbon transport, is a key factor in catalysing the success of Chinese EV manufacturers in Europe.

- The U.S. response includes the Inflation Reduction Act (IRA) of 2022, supporting domestic production which contrasts with the EU's slower response to competitive pressures (notably a tariff increase introduced as late as July 2024). Addendum: Since the Draghi report was published two months before Donald Trump’s election, it does not contain any predictions on how this protectionist stance is likely to escalate and impact car manufacturers from countries outside the U.S. from January 20, 2025.

Solution: SDVs and AI as Transformation Drivers

The report highlights Software-Defined Vehicles (SDVs), together with Artificial Intelligence (AI), as one of the key transformation drivers, as outlined in point 3 below:

- A shift in demand towards third markets away from Europe towards emerging economies such as China

- The rise of electric vehicles (EVs), with the market share of EVs expected to reach 30% in 2026

- Integration with the digital value chain, i.e. SDVs, with electronics and software expected to represent up to 50% of a car's value in 2030 and AI playing an increasingly significant role in future vehicles while requiring new skills on the labour market.

- Integration with the mobility value chain, i.e. reacting to new business models such as car sharing, new financing models, and energy services, requiring zero and low-emission cars (20% expected by 2030) and refuelling infrastructure

- Integration with the circular economy value chain, i.e. re-using, recovering, recycling used materials such as batteries.

Strategic Proposals

The chapter concludes with ten proposals aimed at addressing the decline in EU competitiveness within the automotive sector. From an SDV and open source perspective, several key terms stand out:

- a call for “standardisation” (proposal 4)

- the concept of a “data ecosystem” (proposal 7)

- an emphasis on “innovative areas” such as “software-defined vehicles” (proposal 8)

- “level[ling] the global playing field” (proposal 10).

Standardisation

On standardisation, the paper details (p. 154):

“Common standards are essential to benefit from economies of scale and connectivity in the Single Market, and to create exemplary standards with global range. Standard setting should involve different stakeholders, including industry, scientists, and relevant NGOs in the regulatory process to establish comprehensive and inclusive standards.”

Notably, apart from consistent regulation, a unified protocol for Vehicle-to Charging Point communication is recommended, as well as standardised cybersecurity, data formats, programming languages, and data exchange protocols.

What the paper does not mention at this point, but is obvious: open source ecosystems such as the Eclipse SDV Working Group can help achieve standardisation in the automotive industry by providing a collaborative platform where stakeholders can define, develop, and adopt interoperable frameworks, protocols, and interfaces in a collaborative, transparent, vendor-neutral and cost-effective manner.

Data Ecosystems

On data handling for AI use cases, the paper recommends “[d]ata and system interoperability and common standards for data sharing” (p. 155). What could be a more secure way of exchanging data than dataspaces? Again, the report doesn’t mention this explicitly – in fact, the words “data spaces”/”dataspaces” aren’t mentioned once throughout the entire paper – but in terms of interoperability, data privacy and sovereignty, dataspaces based on open source technologies could be a viable solution, as the EU’s own initiative “Common European Data Spaces” suggests.

SDVs

In the present chapter, Software-Defined Vehicles are mentioned as one out of three key areas that the “EU could consider supporting.” In addition, it is stated that “scale, standardisation, and collaboration will make a difference” in the automotive industry (p. 156), implicitly citing some of the objectives and values of SDV consortia such as the EU’s FEDERATE initiative.

Levelling the Playing Field

Regarding the last proposal for the automotive industry, the paper recommends levelling the global playing field through “technical harmonisation and standardisation at the highest global level” (p. 156), among other measures. Specifically, aligning with the regulations established by the UNECE World Forum for Harmonisation of Vehicle Regulations and the WTO Technical Barriers to Trade Committee is highlighted as essential.

This emphasis on global technical harmonisation and standardisation resonates strongly with the principles of global collaboration within an open source ecosystem. Regarding regulatory requirements, international open source consortia such as the Open Regulatory Working Group could help address industry needs both in Europe and beyond. By adopting such harmonised approaches, the automotive industry can leverage the openness and scalability of an open source ecosystem to drive innovation within the EU while maintaining compliance with international standards and regulation.

Disclaimer: While we read and analysed the report through the lens of SDV and open source stakeholders, the report in its entirety is well worth perusing. It also contains chapters on digitalisation and advanced technologies, computing and AI, and semiconductors.

*Interestingly, the word “open source” is only mentioned once (“open-source”, p. 83) in the entire section of the report.